Are you feeling lost on the long road to a financially secure future? Don’t fret, it happens to the best of us! Choosing a suitable investment option can be exhausting and needs careful consideration. Let’s return to one of the most prominent debates in the investment world: choosing between SIP or Lump sum investments!

Think of it like this: imagine you have decided to go on a road trip throughout the country! Do you save up for diesel and keep filling up your tank throughout the journey at regular intervals(SIP) or do you save up for a full tank at the beginning and fill it up in the starting(LUMPSUM)? It can be confusing, right

Both investment options can be equally inviting from an investor’s point of view, but it is crucial to understand which one will suit you the best and invest in the right one! Both SIP and lump sum investments have their pros and cons. In this article, we will dive into them in detail, help you make an informed investment decision, and introduce you to calculators that will help you visualise your journey. Buckle up and explore the right track for your journey with us!

LET’S START FROM THE BASICS!

What is SIP?

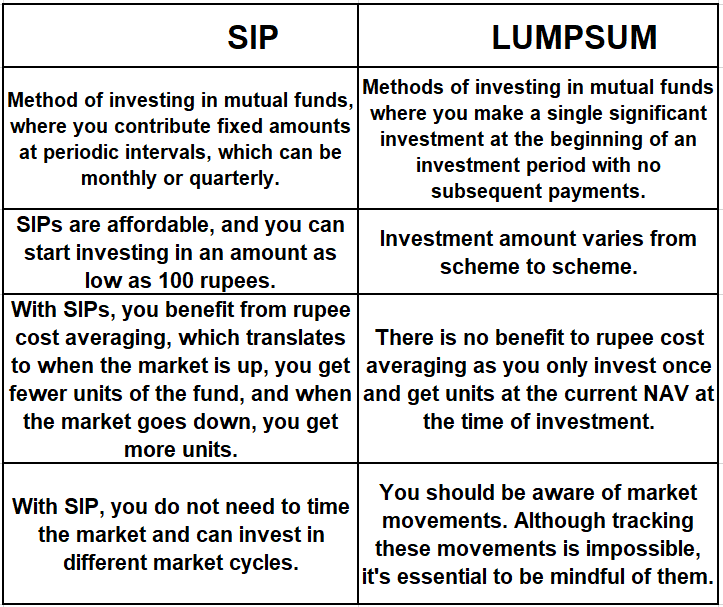

SIP stands for Systematic Investment Plan. It is a popular investment option due to its affordability and flexibility, which allows you to contribute a fixed amount of money at regular intervals to generate long-term wealth over time! It is trendy among all individuals due to a longer investment horizon and minimum savings.

What is Lumpsum?

A lump sum investment is a large one-time payment made at the beginning of an investment period with no subsequent payments. It is a single large corpus created for several purposes, such as retirement plans, investments, insurance premiums, and much more!

DIFFERENCES BETWEEN SIP AND LUMPSUM INVESTMENT!

SIP Vs Lumpsum: Which Is A Better Mode Of Investing?

Both investment routes perform differently in different phases of the market. There is a possibility that the market may correct immediately after you invest your lump sum amount. In this scenario, your average buy price of a unit would have been lower under the SIP route. To put it in a more straightforward way, had you invested via SIP in a falling market scenario, you would have been able to buy more units of the mutual fund for a lower price.

However, to evaluate them over the long term, we did a simple exercise,

We looked at the NIFTY 50 data and analysed the returns you would have earned had you invested a lumpsum at the beginning of the period vis-a-vis the returns you would have earned on a monthly SIP during the entire period. We can look at the two columns on the right.

Summarising the concept of SIP and lumpsum investment that is now demystified.

What should I choose?

It depends on your financial goals, risk appetite, market conditions, and investment horizon. However, here are some general points to consider when choosing between the two modes of investing in mutual funds:

- SIPs are more suitable for beginners or those who have a regular income and want to invest in a disciplined manner. It helps you average the cost of buying units and benefits from the power of compounding over time.

- SIPs can also reduce the impact of market volatility and emotional bias on investment decisions.

- Lumpsum investments suit experienced or savvy investors who know investing well. They can help you take advantage of favourable market conditions and generate higher returns in a shorter period. However, these investments are also riskier.

- You can also combine SIP and lumpsum methods to optimise your portfolio performance. For example, you can start with a lumpsum investment when the market is low and then continue with a SIP to maintain your exposure and accumulate more units. Alternatively, you can start with an SIP and then make additional lumpsum investments when the market dips or you have surplus funds.

Things to Consider Before Investing

Before investing via SIP or lumpsum, you should consider various factors. These factors can help you make the right investment decisions, which can help you achieve your financial goals. Here are some of the factors that you should consider:

Investment Amount

SIP becomes suitable if you have a regular income flow. For example, if you are salaried, SIP is ideal as you can invest some of your income regularly. However, if you have idle cash, then you can prefer to invest via lumpsum.

Financial Goals

If you have a long-term goal such as wealth creation, retirement planning, children’s education, etc., SIP is the best option. If you want to know whether the SIP will be able to fulfil your financial goals, then you calculate your SIP return using the SIP calculator.

However, if you have idle cash in your bank account and want to invest your funds in various asset classes, then you go for lumpsum investment in mutual funds. It will help you earn market-linked returns, which will be far better than the interest earned from traditional methods like your savings accounts and fixed deposits. If you want to calculate your lumpsum return, then you can use the lumpsum calculator to know the future value of your investment.

Type of Fund

Equity funds are highly volatile and, hence, are affected by market swings. Hence, SIP is an ideal option in this type of fund as it is less affected due to rupee cost averaging. On the other hand, debt funds are least impacted by the market movements.

ON A PARTING NOTE…

In conclusion, lump sum or SIP investing has its advantages and is suitable for various investors at various times.

However, one must be aware of the distinction between SIP and Lumpsum. Therefore, it is always advised to start investing early to benefit from the power of compounding in the long run. Choose an investment option based on your financial objectives to earn returns on your investment. Now, it is your call to make a choice!

Name: How To Make The Most Of Stock Market Corrections Through Mutual Funds - BFC Capital- Blogs : All Financial Solutions for Growing Your Wealth

says:[…] Also, check out our recent post on “Sip vs. Lumpsum: Choosing Your Investment Roadmap!“ […]